Understanding the Affordable Care Act, Part 1: The Basics

Authors Reflection

As a physician who has spent decades working within the healthcare system, I’ve seen firsthand how insurance design influences patient care. The goal of this series is not to advocate for a particular policy, but rather to explain how the system works and why these issues matter to patients, physicians, and policymakers alike.

Healthcare policy is often discussed in political terms, but for physicians and patients, the practical question is simpler: how does the system actually work? Over the next several posts, I’ll walk through the Affordable Care Act—how it functions, how it changed during COVID, how it is funded, what it looks like for real patients, and what alternatives policymakers are considering.

The Long Historical Road to the ACA

The Affordable Care Act did not emerge in a vacuum. It was the product of decades of political struggle over coverage, cost, and the proper role of government in American medicine. Long before the ACA, presidents of both parties wrestled with the same core questions: should health insurance remain primarily private and employer-based, or should the federal government guarantee broader access; how much should taxpayers subsidize coverage; and can major reform endure if it is enacted on sharply partisan terms? That longer history helps explain both what the ACA achieved and why it has remained so contested.

Truman and the Origins of the Modern Debate

Modern national health reform began with President Harry S. Truman. In 1945, Truman called for a national health insurance fund run by the federal government, and he continued pressing versions of that idea into the early 1950s. His plan never passed, but it framed the modern debate in unmistakable terms: whether access to medical care should depend chiefly on private insurance and employment, or on broader federal guarantees. Truman did not solve the problem, but he made national health insurance a durable political issue.

Johnson and the First Great Breakthrough

The first major breakthrough came under President Lyndon B. Johnson. In 1965, the Johnson administration enacted Medicare and Medicaid through the Social Security Amendments of 1965. Medicare created national health insurance for older Americans and certain people with disabilities, while Medicaid established a joint federal-state program for low-income populations. Those programs did not create universal coverage, but they permanently established that the federal government could finance large-scale health insurance and that health policy would remain central to American politics.

Nixon and the Republican Path Not Taken

President Richard Nixon belongs in this story as well. In the early 1970s, and especially in 1974, Nixon advanced a comprehensive health insurance proposal built around employers, private insurance, and federal protections for people left outside the traditional market. His plan did not become law, but it is historically important because it shows that broad health reform was not solely a Democratic aspiration. There was also a Republican path that sought wider coverage through a mixed public-private model rather than a single national program.

The Clinton Failure and Its Lessons

The next major turning point came during the Clinton administration. In 1993 and 1994, President William Clinton made health reform a central domestic priority, with Hillary Clinton serving as the public face of the effort. The proposal was sweeping, ambitious, and politically difficult. It ran into resistance from industry groups, strategic and legislative problems inside Washington, and declining public support as the plan became increasingly associated with partisan conflict and governmental overreach. By the summer of 1994, the effort had collapsed. That failure mattered enormously because it taught later reformers that health legislation had to be structured more carefully, sold more effectively, and moved through Congress with tighter political discipline.

The ACA and the Burden of Partisan Passage

The ACA emerged from that history, but it did so on sharply partisan terms. The Senate passed the Patient Protection and Affordable Care Act on December 24, 2009, by a 60-39 vote (with every Democrat and both Democratic-caucusing independents voting in favor, no Republicans voting yes, and one Republican not voting), and the law became identified from the start as a Democratic achievement rather than a bipartisan settlement. That was one of its greatest political burdens. Whatever its policy merits, it entered public life without the broad cross-party legitimacy that often helps major social legislation endure. That weakness shadowed the law from the beginning and shaped nearly every major fight that followed.

The Supreme Court and the Shaping of the Law

The Supreme Court did not merely review the Affordable Care Act; it played a decisive role in determining what the law would actually become. In NFIB v. Sebelius (2012), the Court upheld the ACA’s individual mandate, but only by construing it as a tax rather than as a command enforceable under the Commerce Clause. That alone was a major rescue of the statute. At the same time, however, the Court placed an important limit on the law by ruling that Congress could not compel states to expand Medicaid by threatening their existing Medicaid funding. As a result, Medicaid expansion became effectively optional for the states, and one of the ACA’s central coverage provisions was transformed from a uniform national rule into a patchwork system that varied by state.

The Court intervened again in King v. Burwell (2015), when challengers argued that premium subsidies should be available only on exchanges established by individual states, not on the federal exchange used by many states. Had that argument prevailed, subsidies would have disappeared for millions of Americans in federally facilitated marketplaces, undermining one of the law’s central affordability mechanisms and threatening serious disruption in the insurance markets. The Court rejected that reading and preserved the subsidies, effectively protecting the ACA's operational core.

A third major challenge came in California v. Texas (2021). After Congress reduced the tax penalty for failing to obtain insurance to zero, opponents argued that the individual mandate could no longer be justified as a tax and that the entire ACA therefore had to fall with it. The Court declined to reach that broader constitutional question because it found that the plaintiffs lacked standing to sue. That ruling again left the ACA in place. By that point, the pattern was unmistakable: the Court had repeatedly become the institution asked to decide whether the law could function, how far it could reach, and whether it would survive at all.

Taken together, these cases show that the ACA was not simply enacted in 2010 and then left to operate on its own. It was repeatedly tested in court, repeatedly narrowed or stabilized through judicial interpretation, and repeatedly forced to defend its constitutional and statutory foundations. In practical terms, the Supreme Court helped convert the ACA from a contested legislative achievement into a durable—though still politically disputed—part of the American health-care system.

Trump, McCain, and the Limits of Repeal

President Donald Trump’s first administration made repeal a central goal, and in 2017, Republicans came close to dismantling major parts of the law. The decisive moment came when Senator John McCain voted against the so-called “skinny repeal.” What made that vote especially significant was not that McCain had embraced the ACA. He had not. His objection was more procedural and institutional: he did not want one divisive partisan health-care law replaced by another rushed partisan measure. That argument resonated because it exposed the same structural weakness that had dogged the ACA from the start—health reform in the United States is hard to make durable when passed on one-party terms alone.

COVID-Era Expansion and Renewed Fiscal Questions

The COVID era added another major layer. Rather than replacing the ACA, Congress temporarily made it more generous by expanding premium tax credits, lowering what many consumers had to pay, and extending help beyond the old subsidy cliff. Those changes improved affordability for many households and broadened the law’s reach into the middle class, but they also increased federal spending and revived the old argument over who ultimately bears the cost of more generous coverage. KFF reports that those enhanced credits were later extended through the end of 2025, after which they expired, underscoring again how dependent this policy area remains on continuing political support.

Seen in that full context, the ACA was not the beginning of modern health reform, and it will not be the end of it. From Truman to Johnson, from Nixon to Clinton, from Obama to Trump, and through repeated Supreme Court battles, the history of American health policy has been a long struggle to balance access, cost, markets, and government power. History does not reduce the controversy surrounding the ACA, but it does explain why that controversy was almost inevitable.

What the Affordable Care Act Was Designed to Do

The Affordable Care Act was passed in 2010 with the goal of expanding access to health insurance, improving the quality of coverage, and protecting consumers from some of the most common problems in the private insurance market. Before the law, people with pre-existing medical conditions could be denied coverage or charged far more for it, young adults often lost coverage when they aged out of family plans, and many policies offered narrow benefits while exposing patients to high out-of-pocket costs. Insurers could also impose lifetime limits on coverage, leaving people with serious illnesses financially vulnerable even if they had insurance.

The ACA changed those rules in important ways. Insurance companies must now accept applicants regardless of medical history, and marketplace plans must include a standardized set of essential health benefits such as hospitalization, prescription drugs, preventive care, maternity care, and mental health services. The law also prohibited lifetime dollar caps on essential benefits, limited annual caps in most cases, required many preventive services to be covered without cost-sharing, and allowed young adults to remain on a parent’s health plan until age 26. In addition, the ACA created online insurance marketplaces where individuals and families can compare plans and purchase coverage, often with income-based subsidies that make premiums and out-of-pocket expenses more affordable. Together, these reforms did not eliminate all of the system’s problems, but they established a much stronger baseline of protection and access for millions of Americans.

How the ACA Marketplace Works

The ACA marketplace functions much like an online shopping platform for health insurance. Consumers can compare plans offered by private insurers and choose coverage that best fits their needs and budget.

Plans are generally organized into four “metal tiers”:

Bronze – lower monthly premiums but higher deductibles

Silver – moderate premiums and cost sharing

Gold – higher premiums but lower out-of-pocket costs

Platinum – the most comprehensive coverage

One of the key features of the ACA is the use of federal subsidies that help reduce the cost of insurance premiums for most marketplace enrollees. These subsidies are based primarily on income and are paid directly to insurance companies to lower the monthly price consumers see.

The Premium vs Deductible Tradeoff

Choosing a health insurance plan often involves balancing monthly cost against financial protection when care is needed. Plans with lower monthly premiums typically require patients to pay more out of pocket before insurance begins covering most medical expenses. This amount, called the deductible, can be several thousand dollars in many lower-premium plans. In contrast, plans with higher monthly premiums generally have lower deductibles, meaning the insurer begins paying for care sooner. In practical terms, lower-premium plans may work well for people who expect to use little healthcare during the year, while higher-premium plans can provide better financial protection for individuals who anticipate regular medical visits, prescriptions, or potential hospital care. The key tradeoff is deciding whether it makes more sense to pay less each month but assume more financial risk if illness occurs, or to pay more upfront in exchange for greater coverage when healthcare is needed.

Coverage has Expanded Dramatically

Today, more than 24 million Americans receive insurance through ACA marketplaces, making the program an important component of the U.S. healthcare system. For many individuals—especially those who are self-employed or work for small businesses—the marketplace is the primary way to obtain private health insurance.

At the same time, important questions remain about affordability, government spending, and the program's long-term sustainability.

Eligibility and Coverage Costs

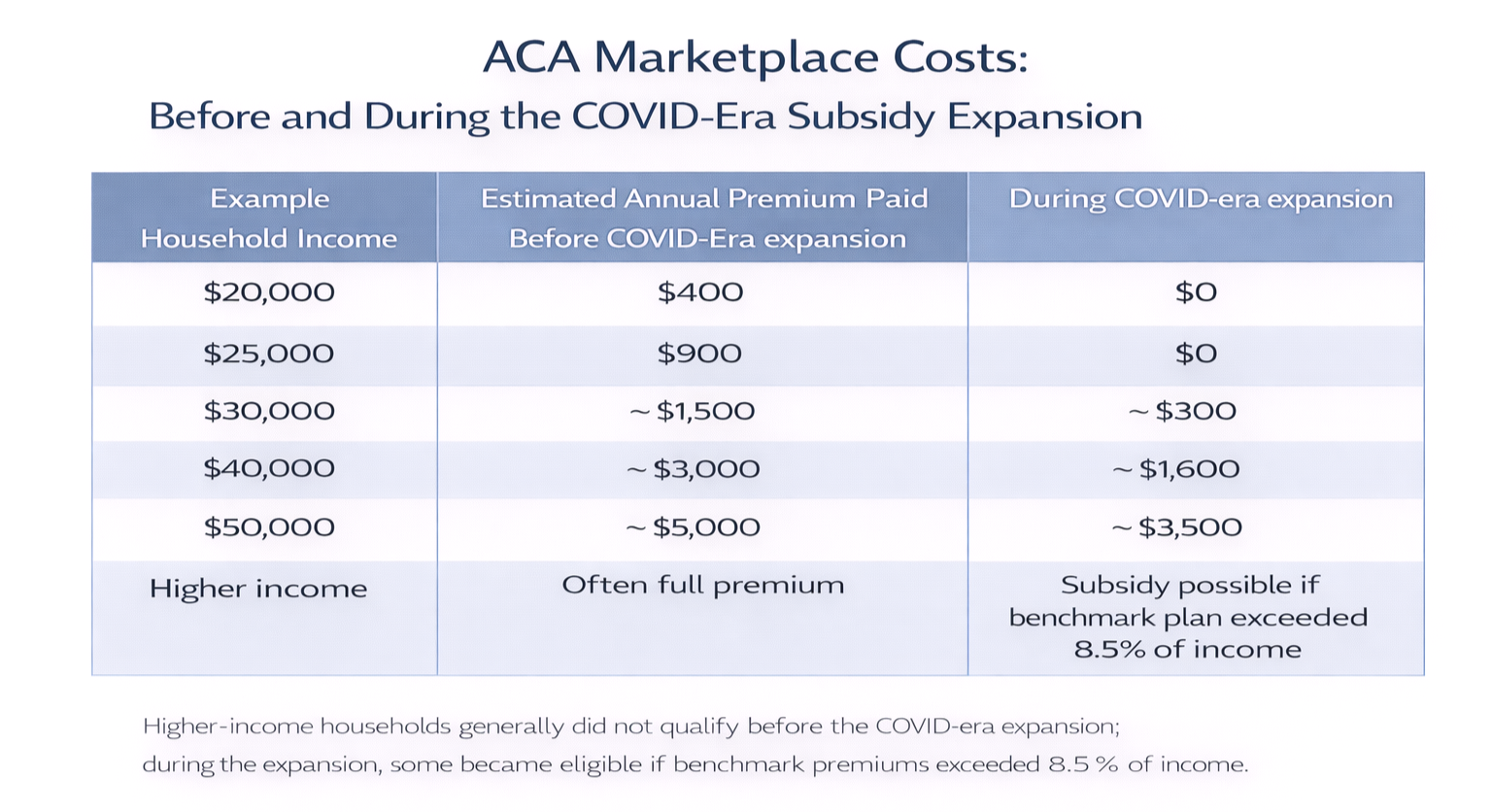

One of the clearest ways to understand the impact of the COVID-era ACA changes is to look at what consumers were expected to pay for benchmark marketplace coverage at different income levels. The example below oversimplifies coverage for clarity.

The table is intended to show consumer cost, not the total price of insurance and not the subsidy itself. Under the ACA, premium tax credits were designed to limit what eligible enrollees had to pay for a benchmark Silver plan, with the federal subsidy covering the difference between that required contribution and the actual premium. Before the COVID-era expansion, assistance was available on a sliding scale, but many households still faced meaningful premium costs, and people above the prior income cutoff often had to pay the full price of coverage. During the COVID-era subsidy expansion, that formula became more generous. Lower-income enrollees could often obtain benchmark coverage for no premium at all, middle-income households saw their required contributions fall, and some higher-income households became newly eligible for assistance if premiums exceeded a fixed share of income.

These examples are necessarily approximate. Actual premiums vary by age, location, household size, tobacco status, and the cost of the benchmark plan in a given market. Even so, the overall pattern is important and accurate: the COVID-era changes materially lowered the expected cost of coverage for many marketplace participants and temporarily softened one of the ACA’s long-standing weaknesses—the sharp subsidy cutoff that had left some consumers facing very high premiums despite being insured through the same system. The tradeoff, however, was significant. More generous subsidies meant substantially higher federal spending, shifting more of the cost of private insurance onto the government. Supporters viewed that as a necessary price for broader affordability and coverage stability, while critics argued that it increased fiscal pressure, added to the long-term burden on taxpayers, and risked making the system more dependent on continued federal subsidies. In that sense, the COVID-era expansion improved affordability for consumers, but it also deepened the central policy question of who ultimately pays—and how much.

References

Harry S. Truman Presidential Library & Museum. “The Challenge of National Healthcare.” Accessed March 16, 2026.

https://www.trumanlibrary.gov/education/presidential-inquiries/challenge-national-healthcareCenters for Medicare & Medicaid Services. “History.” February 12, 2026.

https://www.cms.gov/about-cms/who-we-are/historyThe American Presidency Project. “Special Message to the Congress Proposing a Comprehensive Health Insurance Plan.” February 6, 1974.

https://www.presidency.ucsb.edu/documents/special-message-the-congress-proposing-comprehensive-health-insurance-planMiller Center, University of Virginia. “September 22, 1993: Address on Health Care Reform.” September 22, 1993.

https://millercenter.org/the-presidency/presidential-speeches/september-22-1993-address-health-care-reformU.S. Senate. “Roll Call Vote 111th Congress, 1st Session, Vote 396.” December 24, 2009.

https://www.senate.gov/legislative/LIS/roll_call_votes/vote1111/vote_111_1_00396.htmOyez. “National Federation of Independent Business v. Sebelius.” Accessed March 16, 2026.

https://www.oyez.org/cases/2011/11-393Oyez. “King v. Burwell.” Accessed March 16, 2026.

https://www.oyez.org/cases/2014/14-114Oyez. “California v. Texas.” Accessed March 16, 2026.

https://www.oyez.org/cases/2020/19-840

Looking Ahead

In the next post, we’ll examine how the COVID pandemic dramatically changed the ACA marketplace, leading to record enrollment and significant increases in federal subsidies.