Understanding the Affordable Care Act, Part 5: Alternative Funding Plans

Alternative ACA Funding Plans: The Real Question Is Who Bears the Risk?

The Affordable Care Act has always rested on a difficult bargain: make private insurance more affordable through federal subsidies, regulate the market so that people with medical problems can obtain coverage, and preserve a role for private insurers, employers, states, and individual choice.

That bargain is now under renewed pressure. The enhanced ACA premium tax credits, first expanded during the COVID era and later extended through 2025, expired on January 1, 2026. KFF estimated that expiration would more than double average annual premium payments for subsidized marketplace enrollees, a 114% increase, from about $888 in 2025 to $1,904 in 2026. CMS reported that 22.8 million consumers selected marketplace plans for 2026, but KFF noted that sign-ups were down by more than 1 million compared with the same point the previous year, and that the final enrollment effect would not be clear until paid coverage data became available.

So the debate is no longer simply whether the ACA “works.” It is whether the country wants to keep financing affordability through income-based federal subsidies, redirect that money to consumers more directly, give states more control, create a public insurance alternative, or move toward a much larger national system.

The deeper question is this: who should carry the financial risk–patients, taxpayers, employers, states, insurers, or the federal government?

At a Glance

The ACA funding debate now has three realistic congressional pathways: restore the enhanced premium tax credits, modify them with new limits and safeguards, or redirect some federal support into consumer-controlled accounts such as Health Savings Accounts (HSAs).

The broader policy menu also includes public options, Medicare buy-in proposals, single-payer models, and state innovation waivers. But most of those do not reflect the immediate legislative fight in Congress.

The quiet state-level success story is reinsurance: not dramatic, not revolutionary, but practical. It can lower premiums by helping insurers absorb high-cost claims, and federal pass-through funding can offset part of the state cost.

The partisan reality matters. Democrats are generally trying to preserve and improve the ACA. Republicans have generally tried to repeal, replace, decentralize, or redirect it. That divide shapes what each side calls “success.”

1. Extend or Modify the Current Subsidy System

The most incremental option is to keep the ACA marketplace largely intact while modifying the subsidy structure. That could mean restoring the enhanced premium tax credits, extending them for a fixed period, targeting them more narrowly by income, adding income caps, strengthening eligibility verification, or pairing subsidies with reforms intended to reduce underlying premiums.

For consumers, this approach offers the most continuity. The marketplace remains familiar, the basic structure stays in place, and financial assistance continues to flow automatically through premium tax credits. That matters because ACA affordability is not theoretical; for many households, the subsidy determines whether coverage is realistically affordable.

The fiscal drawback is straightforward: subsidies cost money. CBO estimated that permanently extending the expanded premium tax credit structure would increase federal deficits by $350 billion from 2026 to 2035 while increasing the number of people with health insurance by 3.8 million in 2035.

That tradeoff is the heart of the current debate. Subsidies can protect patients from premium shock, but they do not necessarily reduce the underlying cost of medical care. They mostly decide who pays the bill.

2. Direct Payments, Vouchers, or Consumer-Controlled Accounts

A second approach would move away from subsidies paid through the ACA’s existing premium-tax-credit structure and instead provide consumers with more direct financial assistance—through fixed tax credits, vouchers, Health Savings Accounts, or “health freedom” accounts.

Supporters argue that this gives patients more control, reduces the sense that subsidies are flowing through insurers, and could encourage more shopping and competition. President Trump’s January 2026 healthcare proposal explicitly emphasized sending money directly to eligible Americans, expanding price transparency, holding insurers accountable, funding cost-sharing reductions, and expanding access to HSAs.

The appeal is obvious. Many people distrust insurers, brokers, pharmacy benefit managers, hospitals, and opaque pricing. A direct-payment model promises to simplify the message: give people the money and let them decide.

But the policy mechanics are harder than the slogan. If the federal contribution is fixed and medical costs rise faster than the payment, the financial risk shifts back to consumers. That risk is greatest for older adults, people with chronic disease, low-income patients, and those who need comprehensive coverage rather than a low-premium, high-deductible plan.

KFF’s analysis of Republican HSA-style proposals makes this point clearly. Some proposals would replace part or all of the ACA premium tax credit structure with contributions to HSAs or similar accounts. KFF noted that such approaches may benefit healthier enrollees but could leave sicker people with higher premiums or higher out-of-pocket costs, especially if assistance is tied to bronze plans with large deductibles.

This approach is therefore not simply “more choice.” It is a deliberate shift in risk: less open-ended federal subsidy exposure, more consumer discretion, and potentially more consumer responsibility.

3. What Congress Is Actually Considering

In Congress, the realistic debate has narrowed. Public option, Medicare buy-in, and single-payer ideas remain part of the broader policy conversation, but they are not the main near-term legislative fight.

The first active pathway is restoring the enhanced ACA premium tax credits. Representative Lauren Underwood and Senator Jeanne Shaheen introduced the Health Care Affordability Act of 2025 to make the enhanced premium tax credits permanent. Their legislation reflects the Democratic approach: strengthen the ACA framework and prevent premium increases for marketplace enrollees.

The House passed a three-year extension of the enhanced premium tax credits on January 8, 2026, by a 230–196 vote, with 17 Republicans joining Democrats. That vote showed some cross-party concern about premium increases, especially among members from competitive districts. But the Senate remains the barrier.

The second pathway is a modified bipartisan extension. This is probably the most plausible compromise if Congress acts. Such proposals generally maintain some form of premium assistance but add features Republicans have demanded, such as income caps, shorter duration, minimum premium payments, stronger eligibility checks, fraud controls, or limits on abortion coverage. Reuters reported that Senate negotiators were considering shorter extensions, income limits, and softened abortion restrictions after the House vote.

The third pathway is the Republican consumer-directed model. Senators Mike Crapo and Bill Cassidy introduced the Health Care Freedom for Patients Act, describing it as legislation to lower costs and “give money directly to families to control their own care.” That approach overlaps with President Trump’s stated preference to redirect money away from the existing ACA subsidy model and toward consumers more directly.

The Senate rejected both the Democratic subsidy-extension bill and the Republican HSA-style alternative in December 2025. AP reported that the Democratic bill failed to reach the 60-vote threshold despite support from four Republicans, while the Republican alternative was also blocked.

That leaves the practical congressional question unresolved: restore the subsidies, modify them, or replace part of their value with a more consumer-directed structure.

4. A Public Option or Medicare Buy-In

A third policy pathway—though not the most immediate congressional option—is a public insurance plan that would compete alongside private marketplace plans, or a Medicare buy-in that would allow some adults to enter Medicare before age 65.

A public option is often described as a middle path. It would not eliminate private insurance, but it would create a government-administered plan within the marketplace. The theory is that a public plan could lower premiums through lower administrative costs, broader bargaining power, or Medicare-like provider payment rates.

CBO has emphasized that the effect of a public option would depend heavily on design: provider payment rates, risk adjustment, administrative costs, participation rules, whether the plan is national or targeted to weak markets, and how it affects the benchmark premium used to calculate marketplace subsidies. A low-premium public option could reduce federal subsidies by lowering benchmark premiums, while a public option similar to private plans might have much smaller effects.

A Medicare buy-in is another variant. CBO estimated that lowering the Medicare eligibility age to 60 would increase federal deficits by $155 billion over the 2026–2031 period, enroll about 7.3 million more people in Medicare Parts A and B in 2031, and reduce employment-based coverage by about 3.2 million people.

These options do not eliminate tradeoffs. They change the pricing leverage and the payer. Patients may benefit from more stable public coverage, but taxpayers and providers may bear a greater share of the financial burden.

5. Greater State Flexibility

Another approach is to give states more authority to design their own coverage systems using federal funds. This can occur through ACA Section 1332 State Innovation Waivers, reinsurance programs, state-specific premium assistance, or broader waiver-based experiments.

Under Section 1332, states may pursue alternative coverage strategies while retaining the ACA’s basic protections. CMS states that these waivers must provide coverage that is at least as comprehensive and affordable as coverage without the waiver, cover a comparable number of residents, and not increase the federal deficit.

The strongest argument for state flexibility is that insurance markets vary substantially. Rural states, high-cost states, Medicaid-expansion states, and states with different levels of insurer participation may need different tools. Reinsurance, for example, can reduce premiums by helping insurers pay for unusually high-cost claims.

The risk is unevenness. State flexibility can enable useful experimentation, but it can also lead to variation in benefits, affordability, and consumer protections. If federal funding is capped or reduced, states may inherit more financial risk during recessions, premium spikes, or enrollment surges.

In practical terms, state flexibility works best when it is used to supplement coverage and stabilize markets—not simply to pass fiscal risk from Washington to state budgets or patients.

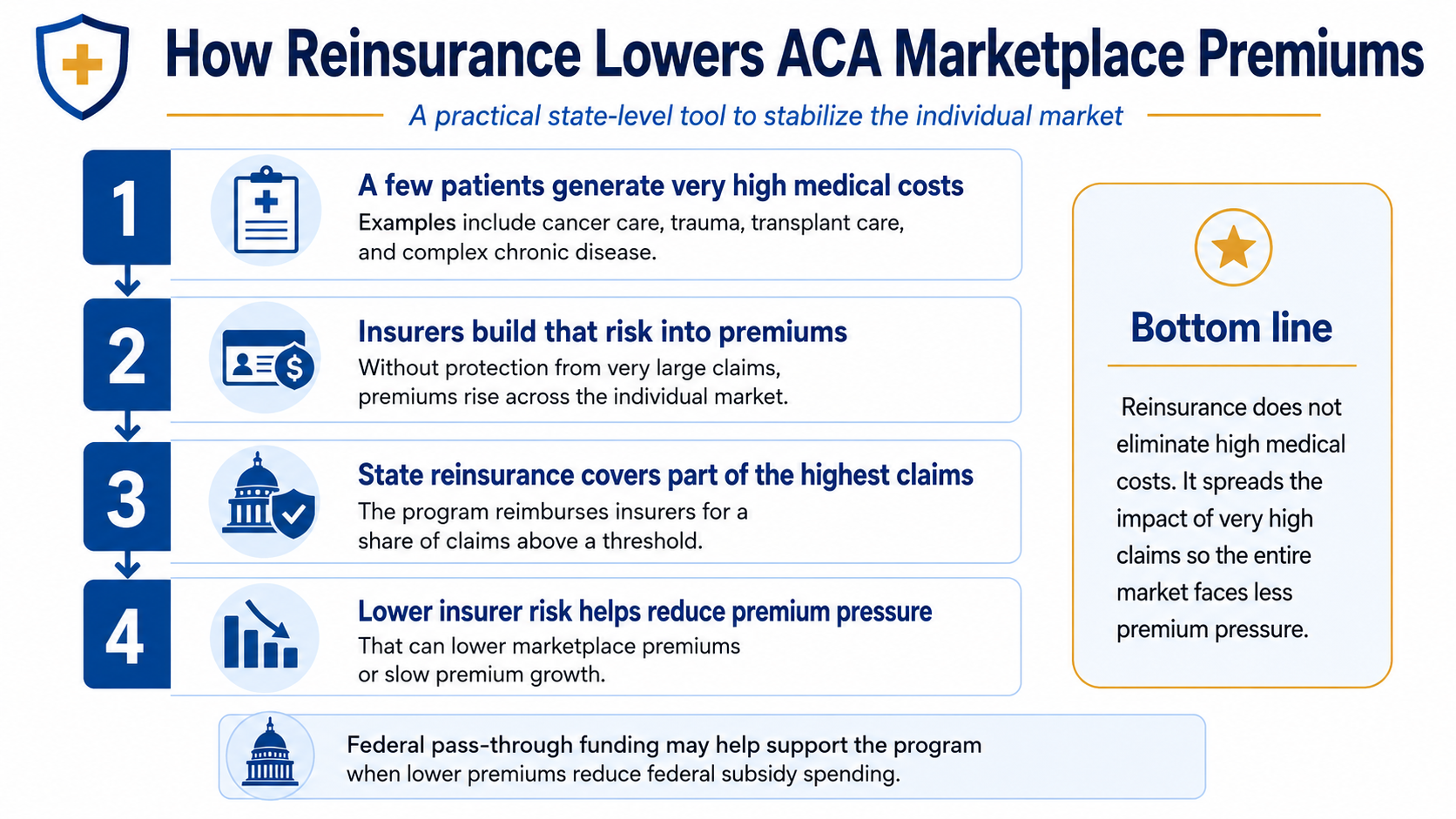

6. The Quiet State-Level Success Story: Reinsurance

Some states have used ACA flexibility creatively without creating a massive new entitlement. The most practical example is state-based reinsurance through Section 1332 waivers.

Reinsurance programs help insurers pay for unusually high-cost claims. That lowers insurer risk, which can reduce premiums across the individual market. The clever financing mechanism is federal pass-through funding: when premiums fall, federal premium tax credit spending may fall as well, and part of those savings can be passed through to the state to help finance the waiver.

KFF’s tracker lists multiple approved state reinsurance waivers, including Alaska, Colorado, Maryland, Minnesota, Oregon, Pennsylvania, Rhode Island, and Wisconsin. These programs generally reimburse insurers for a share of claims above a specified threshold and below a cap, using federal pass-through funding to partially finance the program.

Reinsurance is not a cure for high healthcare costs. It does little to reduce deductibles directly. It does not fix hospital prices, drug prices, physician payment, or administrative complexity. But it is one of the few reforms that has lowered premiums while keeping fiscal exposure relatively bounded.

In that sense, reinsurance may be the least ideological and most practical state-level ACA innovation: not dramatic, not revolutionary, but useful.

7. Single-Payer or “Medicare for All”

At the far end of the spectrum is a single-payer system, often described as Medicare for All. Under this model, one national insurance program would replace most private insurance and finance coverage primarily through taxes.

The conceptual appeal is simplicity: universal coverage, less fragmentation, fewer payer rules, and potentially lower administrative costs. But the transition would be enormous. It would affect employer-sponsored insurance, private insurers, hospitals, physicians, drug pricing, federal taxes, state programs, and nearly every existing financing arrangement in American healthcare.

CBO’s single-payer analysis illustrates the scale. Depending on design choices, CBO projected that federal healthcare subsidies in 2030 would increase by $1.5 trillion to $3.0 trillion relative to current law, while total national health expenditures could either decrease by $0.7 trillion or increase by $0.3 trillion. In other words, single payer could reduce some systemwide costs under certain assumptions, but it would also move a much larger share of healthcare financing onto the federal budget.

That is the central trade-off: less fragmentation and near-universal coverage, but much greater federal responsibility and a major shift in tax financing.

The Partisan Reality Behind the ACA Debate

Any discussion of ACA funding has to acknowledge an uncomfortable political fact: the ACA has been partisan from the start.

The final House vote on the ACA in March 2010 was 219–212. The law passed over unified Republican opposition, and it quickly became one of the defining political dividing lines in American healthcare.

That partisan identity still matters. Democrats passed the ACA, defended it in court, expanded its subsidies during the COVID era, and generally remain invested in proving that the law can be made stable, affordable, and durable. Republicans opposed it at passage, campaigned for repeal-and-replace, and have generally favored alternatives that reduce the ACA’s federal subsidy structure, loosen federal rules, expand state flexibility, or move money into more consumer-directed arrangements.

That does not mean the debate is simply “coverage versus no coverage.” Many Republican proposals do attempt to address affordability, choice, transparency, fraud, and federal spending. But they usually start from a different premise: that the ACA itself is too costly, too centralized, too regulatory, and too dependent on federal subsidies. Democrats, by contrast, tend to see the ACA as an imperfect but functioning framework that should be repaired rather than replaced.

Public opinion reflects that divide. KFF reported in March 2026 that 61% of the public viewed the ACA favorably, but views remained sharply partisan: 90% of Democrats had a favorable opinion of the law, compared with 64% of independents and 32% of Republicans.

This matters because each side defines success differently. For Democrats, success usually means stabilizing the marketplaces, restoring or expanding subsidies, and reducing the number of uninsured. For Republicans, success more often means limiting federal exposure, increasing consumer control, expanding state flexibility, reducing fraud, and reducing dependence on the ACA’s existing subsidy model.

So when Congress debates ACA funding, it is not merely debating spreadsheets. It is debating whether the ACA should be strengthened, modified, or gradually displaced by a different model altogether.

That is why compromise is so difficult. One side is trying to make the ACA work better. The other side is often trying to move beyond it.

Where President Trump’s Approach Fits

President Trump’s current healthcare approach fits most closely within the consumer-controlled funding category, with additional emphasis on price transparency, HSAs, direct payments to individuals, prescription-drug pricing, insurer accountability, PBM reform, and cost-sharing reduction funding.

That approach is politically powerful because it attacks a real frustration: Americans often feel that healthcare dollars flow through insurers, brokers, pharmacy benefit managers, hospitals, and government programs before patients understand what anything actually costs.

But direct funding does not automatically solve affordability. If the amount deposited into an account is too small, if it cannot be used easily for premiums, if it pushes people into high-deductible plans, or if it allows healthier consumers to leave regulated ACA plans, the result may be more choice for some but higher risk for others.

The fair reading is this: Trump’s approach tries to redirect power and money toward consumers. The unresolved question is whether that money would be large enough, stable enough, and sufficiently risk-adjusted to protect people when they are sick—not only when they are healthy.

The Core Tradeoff

Each pathway solves one problem while creating another.

Keeping or expanding subsidies protects patients from premium shock, but increases federal spending. Direct payments and HSAs give consumers more control, but can shift risk to people who need care. A public option may create competition and pricing leverage, but it depends heavily on provider payment rules and federal design. State flexibility encourages experimentation, but can produce uneven protection. Reinsurance can lower premiums, but does not address deductibles or underlying medical prices. Single payer simplifies coverage, but requires a massive shift in federal financing and taxation.

So the ACA funding debate is not really about finding a painless answer. There is no painless answer.

It is about deciding which risk Americans are willing to accept:

higher federal spending, higher patient costs, higher taxes, fewer choices, weaker protections, greater state variation, or more government control.

The honest policy question is not, “Which plan is free?”

It is: Which compromise best preserves affordable coverage, protects patients when they are sick, and remains fiscally sustainable over time?

That is the debate Americans deserve.

References

KFF. ACA Marketplace Premium Payments Would More than Double on Average Next Year if Enhanced Premium Tax Credits Expire. Published September 30, 2025.

Centers for Medicare & Medicaid Services. Marketplace 2026 Open Enrollment Period Report: National Snapshot. Published January 12, 2026.

KFF. ACA Marketplace Enrollment Is Down in 2026—But All of the Data Isn’t In Yet. Published February 5, 2026.

Congressional Budget Office. The Estimated Effects of Enacting Selected Health Coverage Policies on the Federal Budget and on the Number of People With Health Insurance. Published September 18, 2025.

Representative Lauren Underwood. Underwood and Shaheen Introduce Legislation to Permanently Lower Health Care Costs. Published January 9, 2025.

American Hospital Association. House Passes Bill Extending Enhanced Premium Tax Credits. Published January 9, 2026.

Reuters. US House Passes Health Subsidy Renewal in Win for Democrats. Published January 9, 2026.

Senate Committee on Finance. Chairs Crapo, Cassidy Unveil Republican Bill to Make Health Care Affordable, Give Money Directly to Families. Published December 8, 2025.

KFF. The New ACA Repeal and Replace: Health Savings Accounts. Published November 21, 2025.

The White House. Fact Sheet: President Donald J. Trump Calls on Congress to Enact The Great Healthcare Plan. Published January 15, 2026.

Congressional Budget Office. A Public Option for Health Insurance in the Nongroup Marketplaces: Key Design Considerations and Implications. Published April 2021.

Congressional Budget Office. Budgetary Effects of a Policy That Would Lower the Age of Eligibility for Medicare to 60. Published May 16, 2022.

Centers for Medicare & Medicaid Services. Section 1332: State Innovation Waivers.

KFF. Tracking Section 1332 State Innovation Waivers.

Congressional Budget Office. How CBO Analyzes the Costs of Proposals for Single-Payer Health Care Systems That Are Based on Medicare’s Fee-for-Service Program. Published December 10, 2020.

KFF. After 16 Years, Partisans Still View the Affordable Care Act Very Differently. Published March 23, 2026.

Looking Ahead

With this post, we close one policy-focused discussion and shift gears toward a broader civic and constitutional question: how should we think clearly about American democracy in a time of political strain? The next essay, “Democracy Needs Precision, Not Panic,” examines what words like democracy, republic, tyranny, fascism, and constitutional resilience actually mean—and why using them carefully matters. The goal is not to minimize real warning signs, but to separate serious diagnosis from rhetorical escalation.