Understanding the Affordable Care Act, Part 2: How COVID Reshaped ACA Affordability

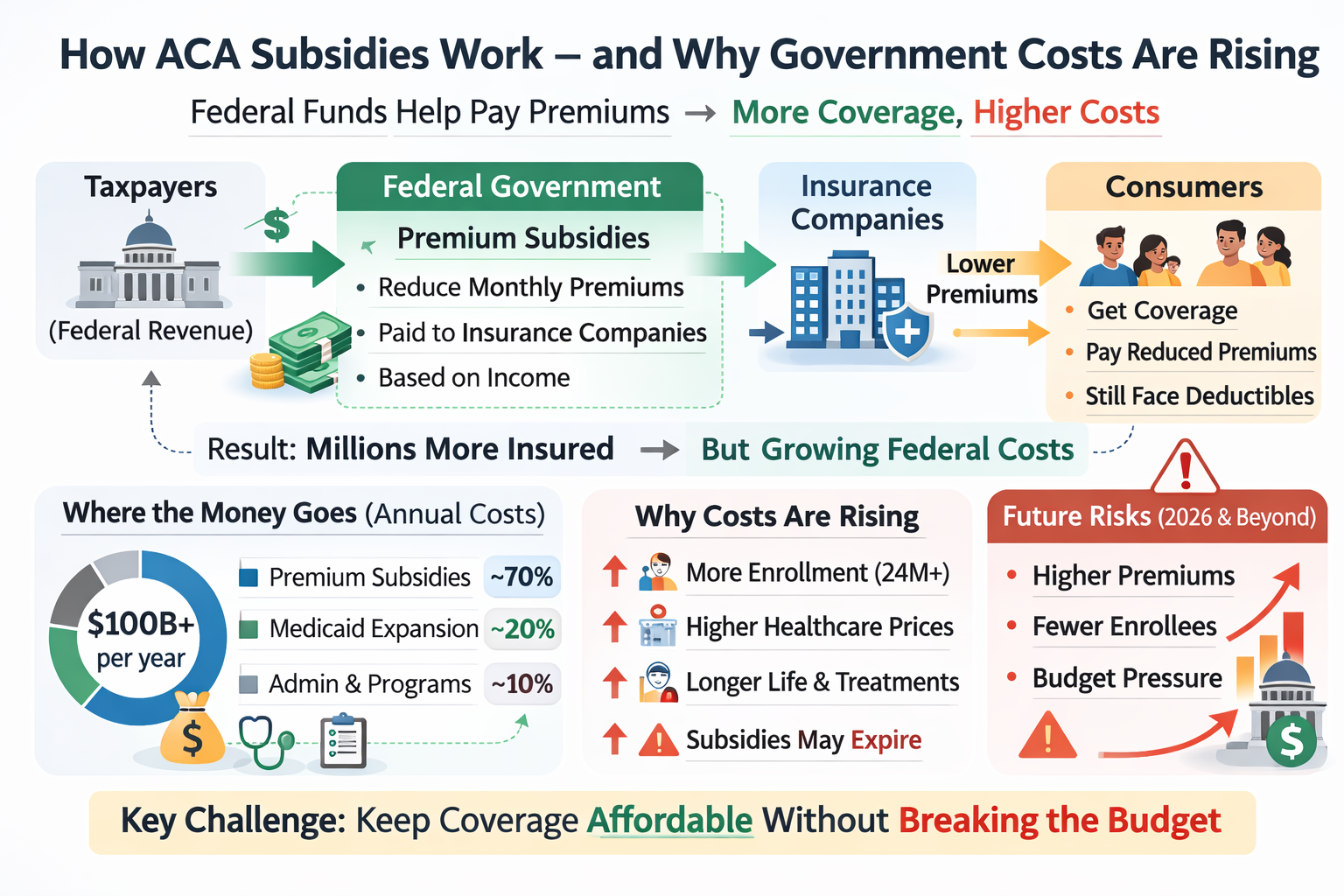

This graphic shows the basic structure of how ACA subsidies work. Federal funds, supported by taxpayers, are used to provide premium subsidies that are paid to insurance companies on behalf of eligible consumers. Those subsidies lower the monthly premiums that individuals and families pay when they purchase coverage through the ACA marketplace. The result is that millions of Americans who might otherwise find health insurance unaffordable can obtain it.

At the same time, the graphic highlights the central tension within the ACA subsidy system: as more people enroll and healthcare costs continue to rise, government costs also rise. In other words, the same mechanism that expands coverage and improves affordability for consumers also increases federal spending. The policy challenge is not simply whether to subsidize coverage, but how to keep coverage affordable without allowing long-term government costs to escalate too rapidly.

How COVID Temporarily Changed the ACA

The COVID-19 pandemic temporarily transformed how the Affordable Care Act worked for millions of Americans. As the economic shock of the pandemic spread in 2020 and 2021, policymakers faced a surge of job losses and disruptions to employer-sponsored insurance. In response, Congress used the existing ACA framework to expand financial assistance and stabilize coverage. The result was not a new system, but a temporary expansion of the ACA’s subsidy structure designed to make marketplace insurance more affordable and accessible during a period of economic uncertainty.

The most important policy change came with the American Rescue Plan (ARP) of 2021. That legislation substantially increased premium tax credits for people purchasing insurance through ACA marketplaces. It reduced the share of income that many enrollees were expected to pay toward coverage and expanded eligibility for subsidies beyond the original ACA limits. In practical terms, the ARP made marketplace plans significantly cheaper for many consumers and allowed some people who previously received little or no assistance to qualify for meaningful subsidies.

One of the most consequential changes involved the elimination of the ACA’s “subsidy cliff.” Under the original law, premium tax credits were generally available only to households earning between 100 percent and 400 percent of the federal poverty level (FPL). Individuals whose income rose even slightly above that threshold often faced the full cost of insurance premiums. The ARP temporarily removed this cutoff. Instead, subsidies were structured so that most households would not have to pay more than 8.5 percent of their income for a benchmark marketplace plan. This adjustment extended financial help to many middle-income households that had previously been excluded.

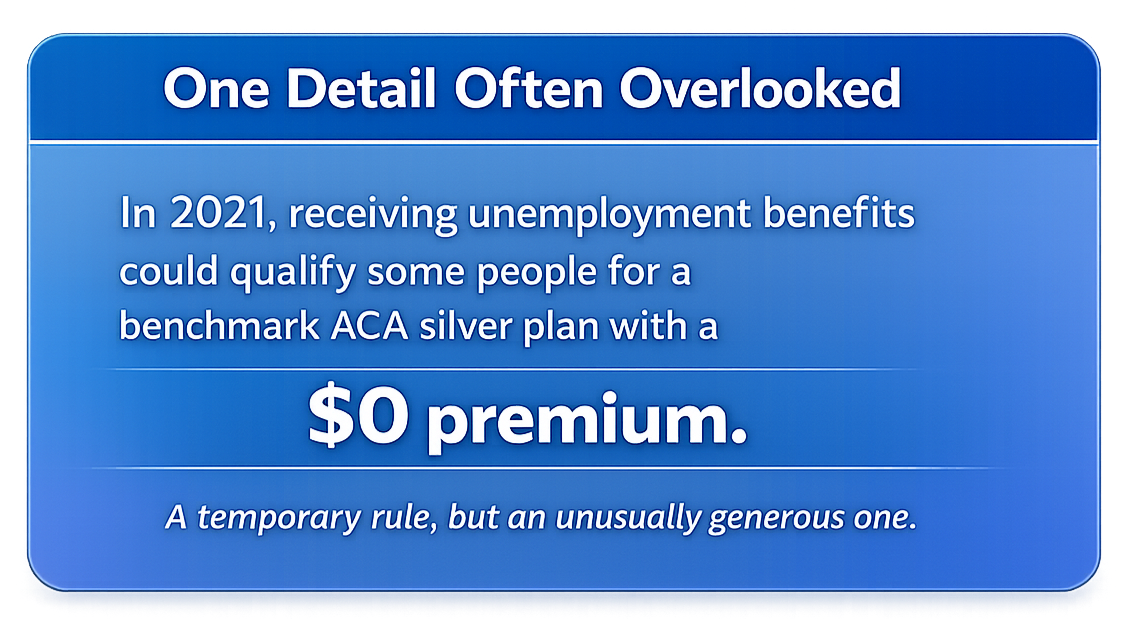

For lower-income enrollees, the changes were even more dramatic. The ARP increased subsidy levels so that many people with incomes between roughly 100 and 150 percent of the federal poverty level could obtain benchmark coverage with little or no monthly premium. Other income groups also saw their expected premium contributions fall. As a result, the effective price of ACA marketplace coverage fell significantly for large segments of the population, and enrollment in marketplace plans increased in subsequent years.

These changes proved politically popular because they made coverage more affordable and expanded access to insurance during a time of national crisis. Many consumers who had previously struggled with high premiums found marketplace plans newly attainable. For policymakers who supported the ACA, the pandemic-era subsidy expansion demonstrated how the law could be used as a flexible platform to expand coverage without replacing the existing private insurance structure.

At the same time, the expanded subsidies came with an important tradeoff: cost. Increasing premium tax credits meant that the federal government assumed a larger share of the cost of private insurance coverage. That translated into higher federal spending and renewed debate about long-term fiscal sustainability. Supporters argued that the increased subsidies improved affordability and reduced the number of uninsured Americans. Critics countered that the policy shifted more costs to taxpayers and deepened the federal government’s financial commitment to subsidizing private insurance markets. Both were correct, more or less.

Although initially enacted as a temporary measure, the enhanced subsidies were later extended through additional legislation, including provisions in the Inflation Reduction Act, which continued the expanded subsidy structure through 2025. As those provisions approached expiration, policymakers again faced a familiar question: should the more generous subsidies become permanent, or should the system revert to the original ACA framework? That debate underscored a recurring theme in American health policy—the tension between expanding coverage and controlling public spending.

In that sense, the COVID-era changes did not fundamentally transform the ACA, but they did reveal both its flexibility and its limits. By temporarily expanding subsidies, Congress showed that the law could adapt to changing economic conditions and political priorities. Yet the fiscal implications of those changes also reminded policymakers that improvements in affordability often come with substantial public costs, ensuring that the debate over the ACA’s future will continue.

Enrollment in the ACA

Another measurable impact of the COVID-era subsidy expansion was a sharp increase in marketplace enrollment. As premiums fell and subsidies expanded under the American Rescue Plan, participation in ACA marketplaces rose steadily. Before the pandemic, marketplace enrollment had stabilized at roughly 11–12 million people annually. By 2024, however, enrollment had climbed to more than 21 million Americans, the highest level since the ACA’s exchanges were created. Much of that growth came from lower premiums for existing enrollees and from middle-income households that had previously been excluded by the subsidy cliff but now qualified for financial assistance. Expanded outreach, longer enrollment periods, and greater public awareness also contributed, but the enhanced subsidies were widely viewed as the most important factor driving the surge.

Early signals following the expiration of the enhanced subsidies in 2026 suggest that the effects may begin to reverse. With the return of the original subsidy structure and the reappearance of the income cutoff above 400 percent of the federal poverty level, many consumers are once again facing higher premiums, particularly middle-income households that briefly qualified for assistance under the COVID-era rules. Early 2026 data show a more challenging marketplace: enrollment remains historically high, but plan selections are down, many consumers report sharply higher costs, and shoppers are shifting coverage choices in response. In that sense, the pandemic did not just temporarily reshape the ACA; it changed expectations about what affordable coverage should look like.

The 2025 Expiration and Government Shutdown

As the enhanced subsidies approached expiration, the debate moved from health policy into the center of federal budget politics. By 2025, the temporary subsidy expansion had become entangled in broader disputes over government spending and fiscal priorities. Supporters of the expansion argued that allowing the subsidies to expire would sharply increase premiums for millions of marketplace enrollees and reverse coverage gains made during the pandemic years. They favored extending the more generous subsidy structure, and some proposed making it permanent. Opponents, however, viewed the expansion as a costly federal commitment that increased long-term deficits and further entrenched government involvement in private insurance markets. As Congress struggled to reconcile those competing priorities during federal spending negotiations, the issue became part of the broader standoff that contributed to the 2025 government shutdown. The dispute illustrated once again how health policy—particularly the question of who pays for coverage—remains tightly intertwined with the nation’s fiscal and political battles.

A Real-World Example of Fiscal Impact

One of the clearest ways to understand the COVID-era ACA subsidy expansions is to separate what they did at the individual level from what they meant for federal spending. For individual enrollees, KFF estimates that in 2024 the enhanced premium tax credits reduced average annual premium payments for subsidized Marketplace enrollees from about $1,593 to $888, a savings of roughly $705 per year. Looking ahead, KFF later estimated that if those enhanced credits were allowed to expire, average annual premium payments for subsidized enrollees would rise from about $888 in 2025 to $1,904 in 2026, an increase of about $1,016 per year.

The budgetary consequences were equally significant. Congressional budget analyses estimate that federal spending on ACA exchange subsidies and related coverage reached roughly $140 billion in 2025, before falling to about $112 billion in 2026, largely because the enhanced subsidies were scheduled to expire. Other fiscal estimates suggest that extending these enhanced subsidies would cost about $30 billion for one additional year and roughly $350 billion over ten years. These numbers help explain why the COVID-era ACA expansions became such an important policy debate: they lowered premiums and boosted enrollment, but they also required the federal government to assume a much larger and more open-ended financial commitment.

The enhanced COVID-era subsidies helped Marketplace enrollees across a wide range of incomes, but their expiration does not affect everyone equally. In many cases, the largest premium increases fall on middle-income and some higher-income households that received substantial temporary assistance under the expanded subsidy rules. Lower-income households may still qualify for significant assistance under the ACA’s original subsidy structure, and some enrollees could reduce premium increases by choosing a less generous plan. As a result, the effects of subsidy expiration vary considerably by age, income, and plan choice.

References

Assistant Secretary for Planning and Evaluation, U.S. Department of Health and Human Services. Health Insurance Coverage, Affordability of Coverage, and Access to Care, 2021–2024. Published January 8, 2025. Available at: original source. Accessed March 28, 2026.

Internal Revenue Service. Questions and Answers on the Premium Tax Credit. Updated November 5, 2025. Available at: original source. Accessed March 28, 2026.

Centers for Medicare & Medicaid Services. Advance Payments of the Premium Tax Credit (APTC) and Cost-Sharing Reductions Overview. Published October 2025. Available at: original source. Accessed March 28, 2026.

Centers for Medicare & Medicaid Services. Marketplace 2024 Open Enrollment Period Report. Published 2024. Available at: original source. Accessed March 28, 2026.

Centers for Medicare & Medicaid Services. Over 24 Million Consumers Selected Affordable Health Coverage in ACA Marketplace for 2025. Published January 17, 2025. Available at: original source. Accessed March 28, 2026.

KFF. Enrollment Growth in the ACA Marketplaces. Published April 2, 2025. Available at: original source. Accessed March 28, 2026.

KFF. Inflation Reduction Act Health Insurance Subsidies: What Is Their Impact and What Would Happen If They Expire?Published July 26, 2024. Available at: original source. Accessed March 28, 2026.

KFF. ACA Marketplace Premium Payments Would More than Double on Average Next Year if Enhanced Premium Tax Credits Expire. Published September 30, 2025. Available at: original source. Accessed March 28, 2026.

Congressional Budget Office. Federal Subsidies for Health Insurance Baseline: 2026 to 2036. Published February 8, 2026. Available at: original source. Accessed March 28, 2026.

Looking Ahead

In the next post, we will examine how the ACA is funded and why the long-term cost of keeping coverage affordable has become such an important public policy question.